SALES: 2018 was a banner year for the restaurant industry. According to the Census Bureau, restaurant sales rose 6% with a menu price (CPI) indexed increase of 2.6%. Even better, for the first time in years,the sales mix between Limited Service and Full Service tilted in favor of Full-Service. Sales of Full-Service restaurants rose 7.9% with a 2.4% CPI increase.

TRAFFIC: The improvement in sales, after deducting menu price increases for the industry, implies traffic and mix improvements of 3.4%. In the Full-Service segment the results imply that traffic and menu mix increased dramatically by 5.5%. In the Limited-Service sector, sales only rose 4.3% with an aggressive CPI menu price increase of 2.8%. This increase could indicate a slowing of the discounting, but more likely indicates higher selling prices of “discounted bundles”. Traffic and mix as a result rose only 1.5%.

MARGINS: Restaurant margins likely expanded in 2018 as PPI increases of All Food was muted at 0.2%. Meanwhile Labor costs increases continue to plague the bottom line. Labor costs rose 5.9% to $175 billion. NRCP calculates industry labor costs from the data available, which fell 80 bps to an average of 24.4%. Deterioration in labor cost comparisons improved throughout the year, but remained negative.

WAGES: According to the Census Bureau, the average wages in the restaurant industry rose to an hourly all-time high of $13.38; up 4.7%. Full-Service wages rose to $14.60 and Limited Service to $11.47. Average hours rose 1.2% overall, with Full-Service up 0.4% and Limited Service up 1.7%.

PRODUCTIVITY: Despite these changes in labor costs, the jump in industry sales aided productivity, which improved by 3.8% overall; 5.7% for the Full-service segment (the best since 1998), while the limited Service segment rose 2.8%, the best since August 2016.

PUBLICLY-TRADED RESULTS:

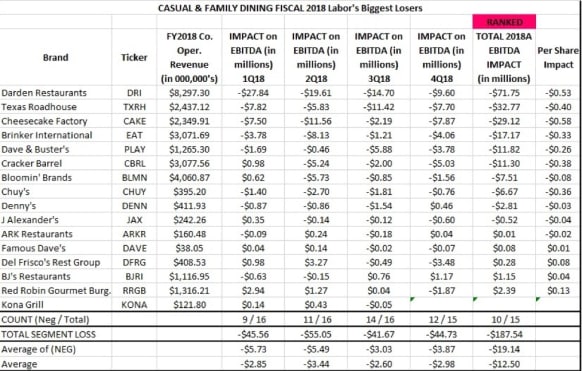

The Casual and Family Dining results remained problematic as the segment lost $187.5 Million in calendar 2018. There were 15 companies that reported quarterly earnings through the full year. Kona Grill has yet to report 4Q18 results, but it is likely to negatively impact the overall results. The quarterly losses for this segment were fairly consistent across the year, with Darden and Texas Roadhouse having the largest increase in labor costs. Just under 33% of companies reported positive labor comparisons. See attached chart:

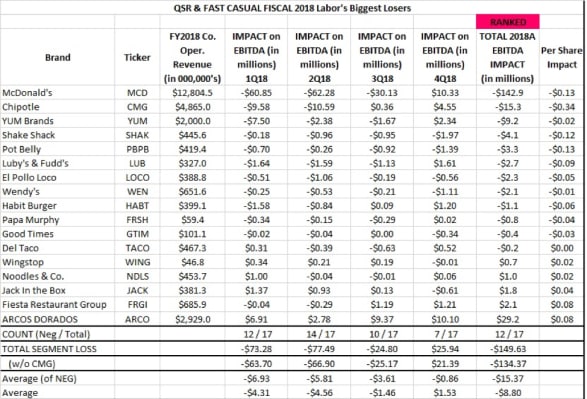

The QSR and Fast Casual Segment spent $149.6 million more in labor costs in calendar 2018. The largest negative impact of $142.9 million occurred at McDonald’s. Interestingly the largest positive impact was at Arcos Dorados, the McDonald’s franchisee in Latin America. The rest of the segment, basically washed each other out.